D-BOX Technology

A triple play idea

D-BOX is what I like to call a “triple play” idea — it has the potential for earnings growth, margin expansion, and multiple re-rating all in one place. It also has other attractive factors such as recurring revenue and activist involvement. Setups like this are rare, but they occasionally show up for those who work hard and are patient.

I had this write-up ready since April, but for various reasons only just posted it now. The stock is reacting well today to the announcement of adding over 70 screens across Cinemark theaters over the next 19 months.1 What I like even more, though, is that the stock barely flinched after the recent news about Trump’s film tariffs a few days ago.

Thesis

D-BOX Technologies (DBO.TO) is a haptic motion technology company based in Quebec. In addition to selling haptic hardware to OEMs that assemble motion chairs for theatres and simulation/training systems, it earns a royalty from each D-BOX motion seat ticket sold. This creates an attractive stream of recurring revenue with minimal costs and significant operating leverage.

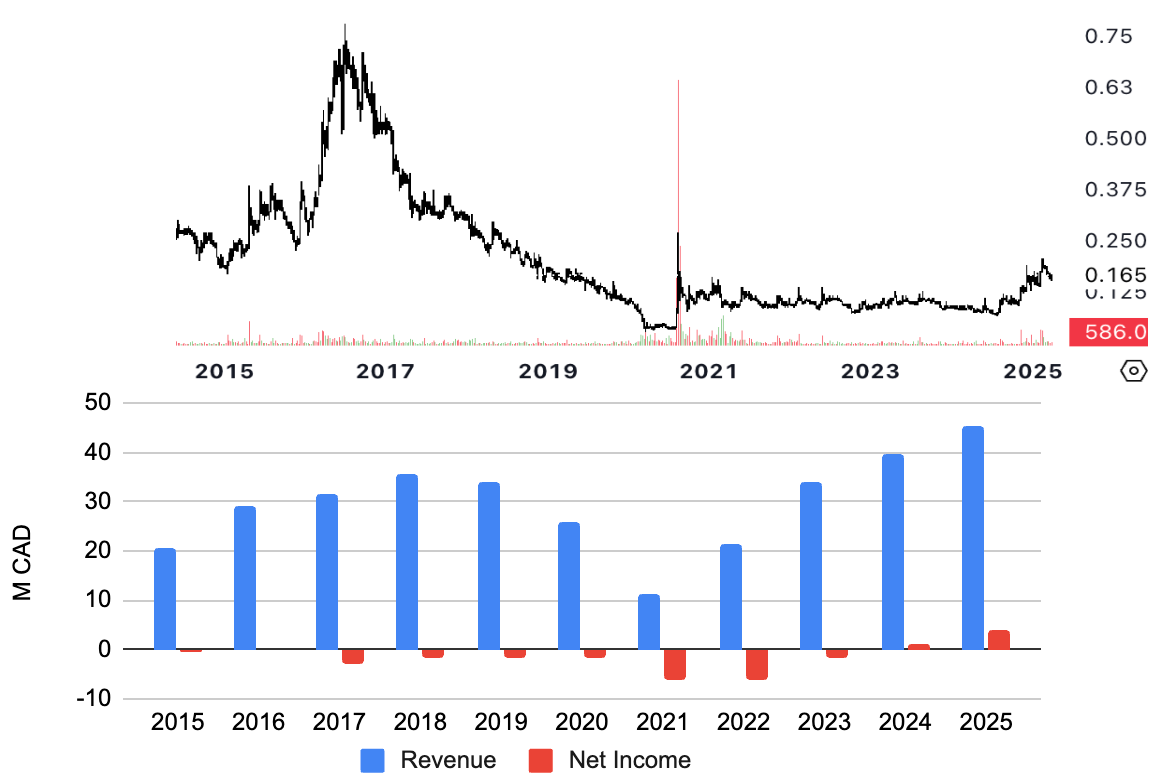

In FY2024, the company reached an inflection point—record-high revenue and its first-ever positive earnings. Momentum remains strong: net income over the past nine months is up 200% compared to FY2024. D-BOX also maintains a clean balance sheet with C$5M in net cash. At a stock price of around C$0.15/share, the company trades at just 7x LTM P/E (after cash) or 5.3x EV/EBITDA. That’s too cheap for a business with expanding margins and substantial growth potential. For context, IMAX Corp trades at 45x P/E and 13x EV/EBITDA with little growth.

Another way to see that D-BOX is undervalued: the stock is currently trading below its 2015 price—even though revenue has doubled and the company has turned profitable since then.

I project D-BOX will reach 1,500 screens within five years—an annual growth rate of 10%, which is very reasonable given their track record (they more than doubled their screen count from 2014 to 2019). This expansion would add approximately C$5M in high-margin licensing fees directly to the bottom line. Applying a conservative 15x P/E multiple (vs. 40x for IMAX), I arrive at a valuation of around C$150M. That implies a 4x return over five years, or an IRR of roughly 30%.

Why this opportunity exists? I can think of three: 1) D-BOX is a micro-cap stock with a market cap under C$40M. It is listed on the TSX and has little analyst coverage. 2) Investors remain pessimistic about the film industry. This sentiment has been exacerbated by events like the streaming wars, COVID-19, and the Hollywood strikes, all of which negatively impacted the industry. 3) It’s still a foreign concept for many investors I talked with.

Technology and Business

Each D-BOX motion system includes three components: an actuator, a controller, and D-BOX motion code. The controller reads D-BOX motion codes—embedded in the video source file as an additional track—and converts them into electrical signals. These signals trigger the actuator (for instance located beneath the seat) to create motion effects that sync with the on-screen action.

D-BOX generates revenue through two primary streams:

The sale of haptic hardware to OEMs that build theatre chairs and simulation/training systems

Licensing of the D-BOX haptic code in theatres

Most of D-BOX’s revenue comes from motion chairs in movie theatres, with a smaller portion from simulation and training. The most intriguing element is the licensing fee (referred to as "royalties" by management), which is essentially a cut of the box office from D-BOX motion seats. This recurring income has almost no associated cost—once revenue reaches a certain threshold, royalties fall directly to the bottom line. In the last twelve months, D-BOX generated C$10M in royalties—with a market EV of about C$30M. Investors may think they're buying a hardware company, but they’re actually getting a software business bundled in.

D-BOX operates in a niche market with notable barriers to entry:

Its haptic technology is patent-protected

Switching costs for theatres are high; alternative motion codes won’t be compatible with D-BOX hardware, requiring replacement of actuators or entire chairs

D-BOX is the only company authorized to produce motion codes for Hollywood films, backed by a decade-long relationship with major studios

D-BOX Motion Seat Experience

For those who haven’t tried motion seating, it’s reasonable to wonder if audiences are willing to pay double for a motion seat. I tried a D-BOX motion seat while watching The Working Man a few weeks ago. I found it distracting at the beginning. I got used to it later, though some of the motion effects still felt unnecessary. However, I suspect the experience would be better for films with lots of action or visual effects.

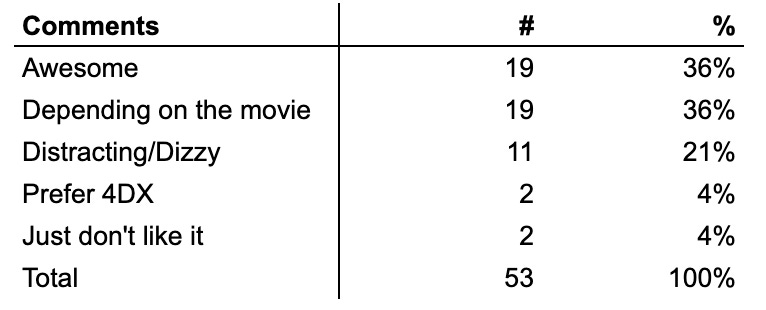

Since my personal experience is certainly not representative, I reviewed every Reddit thread discussing D-BOX experiences. I categorized 50 user comments: 72% were highly positive, though half of those emphasized that the experience depends heavily on the type of movie. Most negative comments mentioned the motion being distracting—though I believe some of these users, including me, might just need some getting used to.

Of course, fifty data points are not statistically significant, but the findings align with my own experience and common sense. I believe D-BOX serves a niche audience—one that values immersive experiences for specific movie genres.

Opex control and Activism

I won’t talk much about D-BOX's gross margin as it has remained stable, around 50%. It dips slightly during periods of high hardware sales but rises when those installations begin generating royalties.

However, operating expenses have long been an issue. D-BOX could have been profitable as early as FY2017 with better cost discipline.

In 2023, Daniel Marks of Stonehouse Capital—holding a 9.6% stake—publicly criticized management and called for a sale of the company:2

"Mr. Marks believes the company's existing theatrical segment is worth $55–70 million or $0.25–0.32/share on a standalone basis... Despite its leading-edge haptic technology, D-BOX remains unprofitable. A post-COVID rebound in the movie industry and opportunities in home gaming are being squandered as D-BOX cannot control expenses and is using right-of-use revenue to fund inefficient operations. Administrative expenses alone increased 35% YoY in Q4 2023."

Although the strategic review led nowhere, Marks succeeded in securing two board seats. Since then, cost control has become a formal part of the business strategy stated in MD&A, and both the Chair and CEO have emphasized shareholder value in their letters. The results are encouraging. D-BOX posted its first positive earnings in FY2024. Operating expenses held steady at C$18.7M—same level from eight years ago. As a percentage of revenue, expenses dropped to a new low of 41%, 10 percentage points lower than a decade ago. That’s impressive considering today's inflationary environment.

Growth Drivers

D-BOX’s theatrical revenue is driven by two key factors: box office performance and penetration rate. Let’s start with the latter.

Penetration is measured by the number of screens equipped with motion seats. Most auditoriums have 2–3 rows of D-BOX seats in prime locations. In the U.S., some auditoriums are entirely D-BOX-enabled. Excluding the COVID period, D-BOX has steadily expanded its footprint—from 400 screens in 2015 to 1,006 screens today. There are 43,000 screens across the U.S. and Canada, so D-BOX’s penetration rate is just ~2%. The growth potential is enormous. I don't see any fundamental reason why each screen couldn’t have at least a few rows of motion seats.

D-BOX also benefits from two secular tailwinds:

1. After years of setbacks—from streaming to COVID to strikes—cinema chains are eager to win back audiences by offering premium experiences that can't be replicated at home. Formats like IMAX, 4D, and D-BOX are part of that strategy.

2. Hollywood is increasingly focused on high-budget blockbusters rich in visual effects—exactly the kind of content best suited to motion seating.

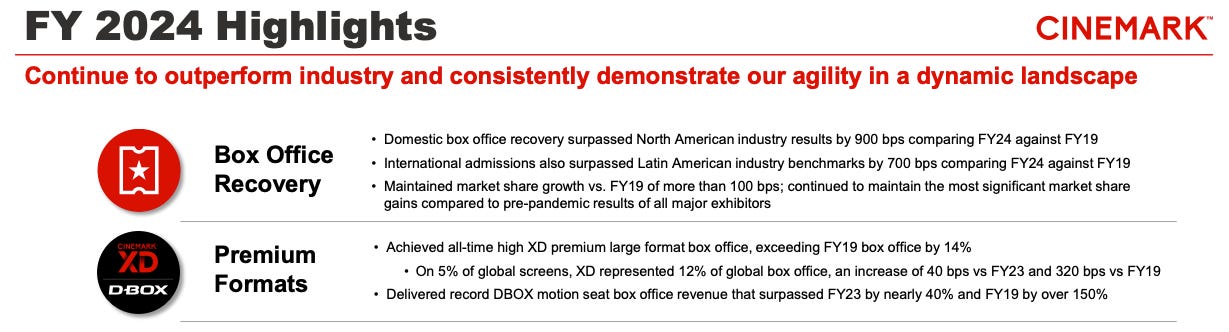

Cinemark, D-BOX’s largest customer, reported a 40% YoY increase in D-BOX seat box office revenue in its latest earnings call and plans further installations. A 10% annual growth rate in penetration is achieved in FY2025 and appears to be sustainable for D-BOX over new few years.

The second growth driver is the box office. Apparently, if fewer people go to the movies, D-BOX’s revenues will suffer. Unfortunately, theatrical attendance has declined from 30+ annual visits per person in the 1930s to around 2 today. COVID accelerated that trend, and it's unclear whether it's a temporary overcorrection or a long-term shift. Many investors believe the theatrical industry is a melting cube.

Many theories exist, but the most compelling explanation for me is the abundance of alternative entertainment options available today. This theory is supported by the finding that, compared to 10 years ago, only those between age 2-24 have lower theatrical attendance.

There’s a silver lining, however, for D-BOX. There is a hedging effect between the two drivers, as a slowdown of the theatrical industry will create more demands of D-BOX motion chairs. Whether the film industry is in terminal decline or poised for a renaissance through embracing new tech is impossible to predict—but historically, widespread pessimism has often proven excessive.

Valuation

I assume D-BOX reaches 1,500 screens in five years—a 10% annual growth rate consistent with FY2025. Assuming box office revenue remains stable and each screen generates similar royalties, that’s an additional C$5M in licensing fees, dropping straight to the bottom line (D-BOX has a C$40M NOL carryforward). Add this to the current C$4M LTM net income, we’re looking at C$9M net income by 2030. Apply a conservative 15x P/E (IMAX trades at 40x), I get a valuation of ~C$150M—representing a 4x return in five years or a 30% IRR.

Notice that my calculation is conservative as I haven't considered potential contributions from hardware sales (which could add C$50M to the top line according to my estimation) and possible growth from the simulation/training segment.

Catalyst

1. Box Office Recovery. A few strong years at the box office could change investor sentiment, leading to re-ratings of companies related to the industry.

2. Shareholder Returns. As D-BOX continues to generate strong cash flow, and their debt expected to be paid off this year, they will start paying dividends or buying back shares. The activist will make sure of this and the company will get re-rated.

The author of this write-up owns shares in the companies mentioned and may purchase or sell shares without notice. This write-up represents only the author’s personal opinions and is not a recommendation to buy or sell a security. No information presented in the write-up is designed to be timely and accurate and should be used only for informational purposes. Readers of the write-up should perform their own due diligence before making investment decisions.

From Cinemark's Q1 earning call: Management seems to be quite optimistic about the movie industry in the next few years. They resumed dividend payment and executed the first share buyback (though more related to the convertible note due in August).

Also found this from the transcript: " the opening weekend of A Minecraft Movie in April just yielded our highest three-day sales of D-BOX motion seats ever."